Understand how a trust functions as a legal structure for managing, protecting, and transferring property over time.

The Structure Behind Every Trust

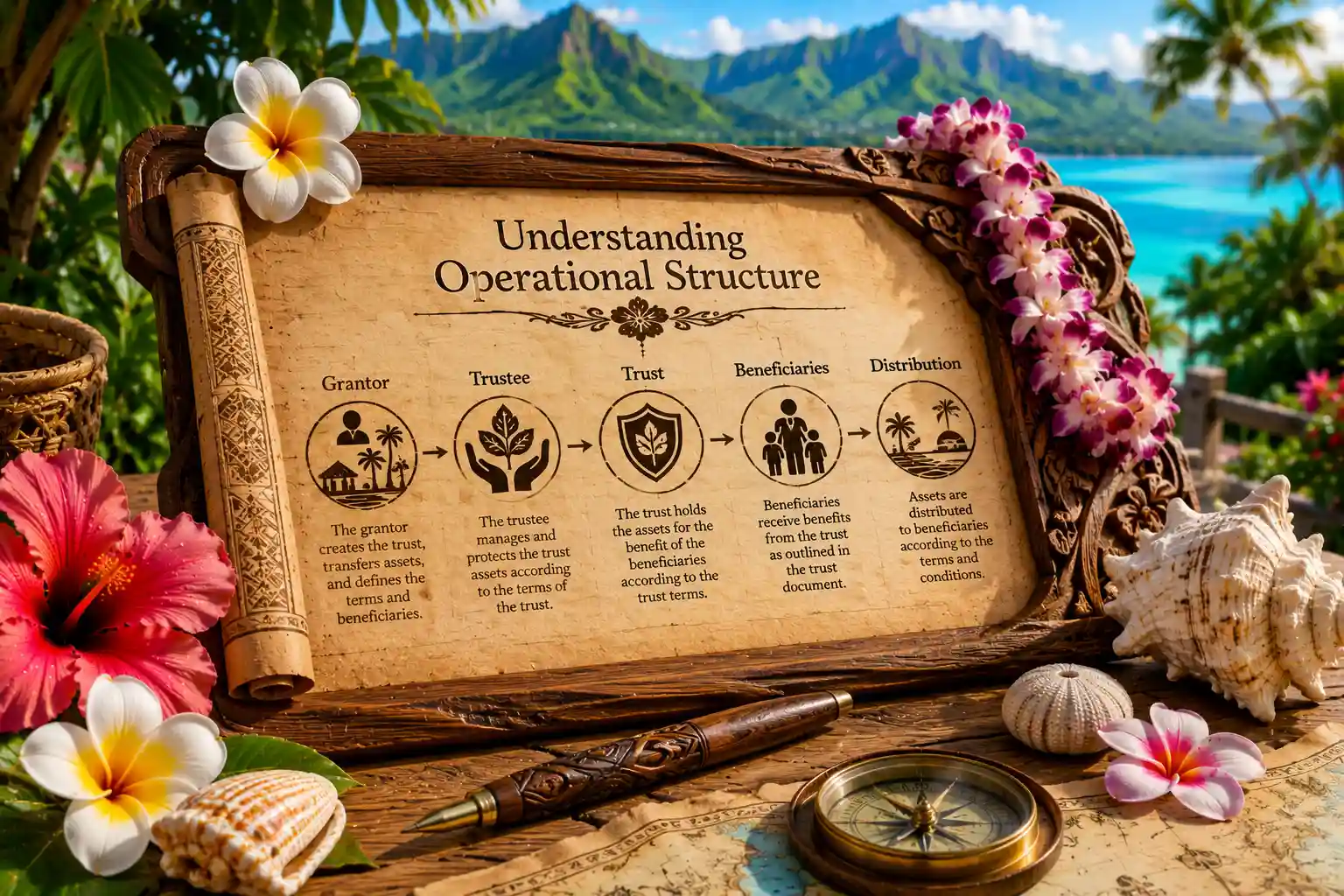

A trust functions by separating legal control from beneficial ownership. The grantor transfers property into the trust, the trustee assumes fiduciary authority over the assets, and the beneficiaries receive the financial benefit according to the terms established within the trust agreement. This separation allows property to continue being managed during incapacity, after death, and throughout long-term administration without requiring direct ownership by the beneficiaries themselves.

The effectiveness of a trust depends heavily on operational coordination rather than the document alone. Assets must be properly transferred into the trust, fiduciary duties must be administered correctly, and trustees must maintain financial oversight, accounting records, and compliance with the trust terms over time. A properly functioning trust creates continuity, preserves administrative stability, and establishes a structured system for managing property across future generations.

Understanding the Operational Structure of a Trust

Operational continuity, fiduciary structure, and trust administration.

Explore the legal and operational framework

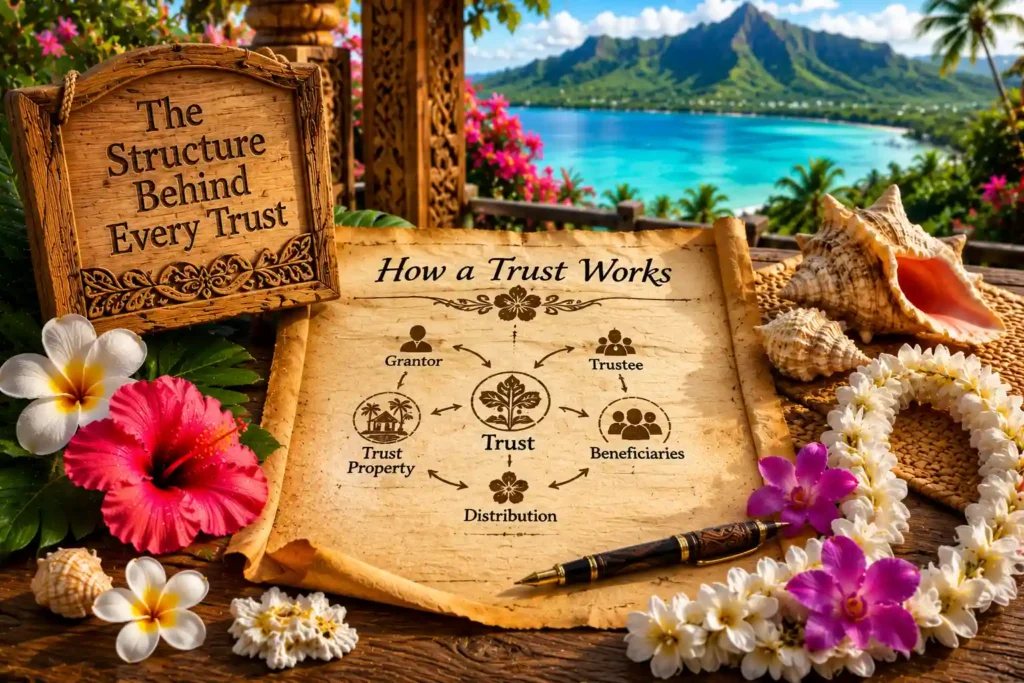

A trust functions through a structured relationship between the grantor, trustee, beneficiaries, and the assets placed inside the trust itself. Each part of the structure carries a distinct legal purpose that affects ownership, control, administration, and long-term succession planning. Understanding these operational mechanics is essential because trusts derive their effectiveness not merely from the document alone, but from how the structure is funded, managed, and administered over time.

A trust separates legal control from beneficial ownership.

One of the foundational legal principles underlying trust law is the separation between legal control and beneficial ownership. Unlike direct personal ownership, where one individual possesses both control over property and the right to personally benefit from it, a trust divides these interests between different parties operating within the trust structure. The trustee typically holds legal title and administrative authority over the trust property, while the beneficiaries retain the equitable or beneficial interest connected to the assets. This separation allows the trust to function as an independent legal relationship capable of managing property according to instructions established by the grantor rather than according to unrestricted personal ownership rights.

The distinction between control and beneficial ownership serves several important operational and legal purposes. Because trustees hold legal authority over the trust assets, they are able to manage investments, administer property, coordinate financial transactions, oversee distributions, and preserve operational continuity on behalf of the trust itself. Beneficiaries, by contrast, generally possess the right to benefit from the assets according to the trust terms without necessarily controlling how those assets are managed on a day-to-day basis. This separation creates a structured governance system designed to preserve stability, reduce administrative disruption, and maintain long-term oversight of the property across changing family and financial circumstances.

This legal structure becomes especially important during periods of incapacity, death, or generational transition. If assets remain personally owned without a trust structure, operational authority may become uncertain once the owner is no longer capable of managing the property independently. A properly structured trust allows the trustee to continue administering the assets without requiring direct ownership by the beneficiaries themselves. Real estate, businesses, investment accounts, and multigenerational property holdings can therefore continue operating under centralized fiduciary management even after the original grantor is no longer able to supervise the system personally.

The separation of control from beneficial ownership also creates fiduciary obligations that distinguish trust administration from ordinary personal ownership. Trustees are not permitted to manage trust assets solely for their own benefit unless specifically authorized by the trust terms and applicable law. Instead, fiduciary duties generally require trustees to administer the trust with loyalty, prudence, neutrality, and good faith on behalf of the beneficiaries and the trust structure itself. This fiduciary framework imposes legal accountability upon the trustee while preserving the beneficiaries’ equitable rights within the administration process.

Ultimately, the division between legal authority and beneficial interest is what allows trusts to operate as long-term continuity structures rather than simple inheritance devices. By separating operational control from personal ownership, trusts create organized systems capable of preserving property, managing assets, and carrying out the grantor’s intentions across future generations. This structure allows trusts to provide continuity, fiduciary oversight, and administrative stability in situations where direct ownership alone may be insufficient to preserve long-term governance and succession planning objectives.

A properly funded trust can continue operating during incapacity and after death.

A trust derives much of its practical value from its ability to continue functioning during periods where the original grantor is no longer capable of managing personal affairs independently. Unlike assets held solely in an individual’s personal name, property that has been properly transferred into a trust structure may continue being administered by the trustee according to the trust terms during incapacity, illness, disability, or after death occurs. This continuity allows financial management, property oversight, and fiduciary administration to continue without requiring immediate court intervention or disruption of operational control. As a result, properly funded trusts often serve as long-term continuity systems rather than merely post-death distribution instruments.

The concept of “funding” a trust refers to the legal transfer of ownership or title of assets into the trust structure itself. Simply signing a trust document does not automatically place assets under trust administration. Real estate deeds, financial accounts, business interests, investment portfolios, and other forms of property generally must be coordinated with the trust through proper ownership transfers, assignments, or beneficiary arrangements. If assets are never transferred into the trust, the structure may exist legally while remaining operationally ineffective because the trustee lacks authority over the property intended to be governed by the trust.

This operational continuity becomes critically important during incapacity because the trust may allow a successor trustee to assume management authority immediately according to the trust provisions. Financial obligations can continue being paid, businesses can remain operational, investments can be supervised, and real estate can continue being managed without the delays frequently associated with court-supervised incapacity proceedings. Families often underestimate how disruptive incapacity can become when authority structures are unclear or when property remains personally owned without coordinated fiduciary systems already in place.

The trust’s ability to continue functioning after death also provides significant administrative stability. Because the trust already holds legal authority over the assets contained within it, successor trustees may continue administering trust property without necessarily requiring probate administration for those specific assets. This can help preserve continuity involving banking relationships, business operations, investment management, and multigenerational property holdings during periods where families are already facing emotional and financial transition. The trust structure therefore allows operational systems to continue functioning despite the death of the original grantor.

Ultimately, the effectiveness of a trust depends heavily upon proper funding and coordinated administration rather than the legal document alone. A trust that has not been properly funded may fail to provide the continuity, authority, and operational protection it was designed to create. When assets are correctly transferred into the structure and fiduciary systems are maintained appropriately over time, the trust becomes capable of preserving management continuity, protecting organizational stability, and carrying out long-term succession objectives across incapacity, death, and future generational transitions.

Trust property must be legally transferred into the trust for the structure to function properly.

One of the most misunderstood aspects of trust planning is the distinction between creating a trust and properly transferring property into the trust structure itself. A trust document alone does not automatically govern all assets owned by the grantor. In order for the trustee to possess legal authority over trust property, the assets generally must be formally transferred, assigned, retitled, or otherwise coordinated with the trust according to applicable legal and financial procedures. Without this transfer process, the trust may exist legally while remaining operationally disconnected from the property it was intended to manage and protect.

The process of transferring assets into the trust is commonly referred to as “funding” the trust. Funding may involve recording new deeds for real estate, changing ownership on financial accounts, assigning business interests, updating beneficiary designations, or coordinating investment accounts with the trust structure. Each category of property may require different transfer procedures depending on the nature of the asset and the laws governing ownership rights. If these steps are neglected or handled inconsistently, important assets may remain personally owned outside the trust despite the grantor’s belief that the estate plan was fully completed.

The legal transfer of property is essential because trustees derive their authority primarily from the trust’s ownership interest in the assets themselves. A trustee generally cannot manage, distribute, refinance, sell, or administer property that was never legally placed under trust control. During incapacity or after death, this operational gap can create significant administrative complications involving probate exposure, banking restrictions, title disputes, or uncertainty regarding fiduciary authority. Families often discover these problems only after a crisis occurs, when the absence of proper funding prevents the trust from functioning as originally intended.

The issue becomes especially significant in estates involving real estate, businesses, investment structures, or multigenerational property holdings requiring ongoing management continuity. A trust designed to preserve operational stability may fail to accomplish its objectives if key assets remain outside the fiduciary structure entirely. Successor trustees may encounter delays accessing accounts, uncertainty regarding ownership, or legal obstacles preventing efficient administration because the property was never transferred properly during the grantor’s lifetime. The operational effectiveness of the trust therefore depends heavily upon consistent coordination between the legal documents and the ownership systems surrounding the assets themselves.

Ultimately, proper funding transforms a trust from a theoretical legal instrument into a functioning operational structure capable of administering property according to the grantor’s intentions. The transfer of assets into the trust establishes the legal authority necessary for trustees to preserve continuity, manage assets, coordinate distributions, and administer the estate efficiently over time. Without proper funding, even a carefully drafted trust may become partially ineffective because the structure lacks legal control over the very assets it was created to govern.

Trusts can preserve continuity for real estate, businesses, investments, and multigenerational property holdings.

One of the primary advantages of a trust structure is its ability to preserve continuity across assets that require ongoing management beyond the lifetime or capacity of the original owner. Real estate portfolios, operating businesses, investment accounts, and multigenerational property holdings often depend upon centralized oversight, financial coordination, and long-term operational stability in order to remain functional over time. When these assets are held solely through personal ownership, incapacity or death may interrupt management authority, delay decision-making, or create administrative uncertainty during periods where continuity is critically important. A properly structured trust helps maintain organized control by allowing successor trustees to continue administering the assets according to predetermined fiduciary procedures.

Real estate holdings are particularly vulnerable to operational disruption when ownership transitions occur without coordinated succession systems already in place. Rental properties, vacation homes, agricultural land, and income-producing real estate often require ongoing payment of taxes, insurance, maintenance obligations, financing arrangements, and vendor contracts regardless of whether the original owner is alive or capable of managing the property personally. Trust structures allow successor trustees to continue overseeing these responsibilities without immediate interruption, helping preserve both the operational integrity and financial stability of the real estate during periods of transition.

Business interests also benefit substantially from continuity planning through trust administration. Many family businesses rely heavily on centralized leadership, operational authority, financial oversight, and long-term strategic management that may become unstable after incapacity or death occurs. A trust can provide an organized framework through which successor trustees or designated fiduciaries continue supervising ownership interests, preserving contractual relationships, maintaining business operations, and coordinating succession planning according to the grantor’s long-term objectives. Without these governance systems already established, businesses frequently face operational confusion, leadership disputes, or financial instability during ownership transitions.

Investment structures and multigenerational property holdings similarly require continuity beyond simple inheritance distribution. Investment accounts may require strategic management, tax coordination, liquidity oversight, and disciplined fiduciary administration over many years. Family property intended for future generations often depends upon organized governance systems capable of balancing present beneficiary interests against long-term preservation goals. Trusts create fiduciary frameworks designed to preserve these assets across changing family circumstances while reducing the likelihood of fragmentation, unmanaged liquidation, or operational collapse following generational transition.

Ultimately, trusts function not merely as inheritance devices, but as long-term organizational systems capable of preserving stability for assets requiring active management and continuity over time. By centralizing fiduciary authority within an ongoing trust structure, trusts allow real estate, businesses, investments, and multigenerational holdings to continue functioning despite incapacity, death, or changing family leadership. This continuity helps preserve operational order, financial stability, and long-term succession planning objectives that may otherwise become vulnerable under direct personal ownership alone.

Fiduciary duties require trustees to act with loyalty, prudence, neutrality, and operational discipline.

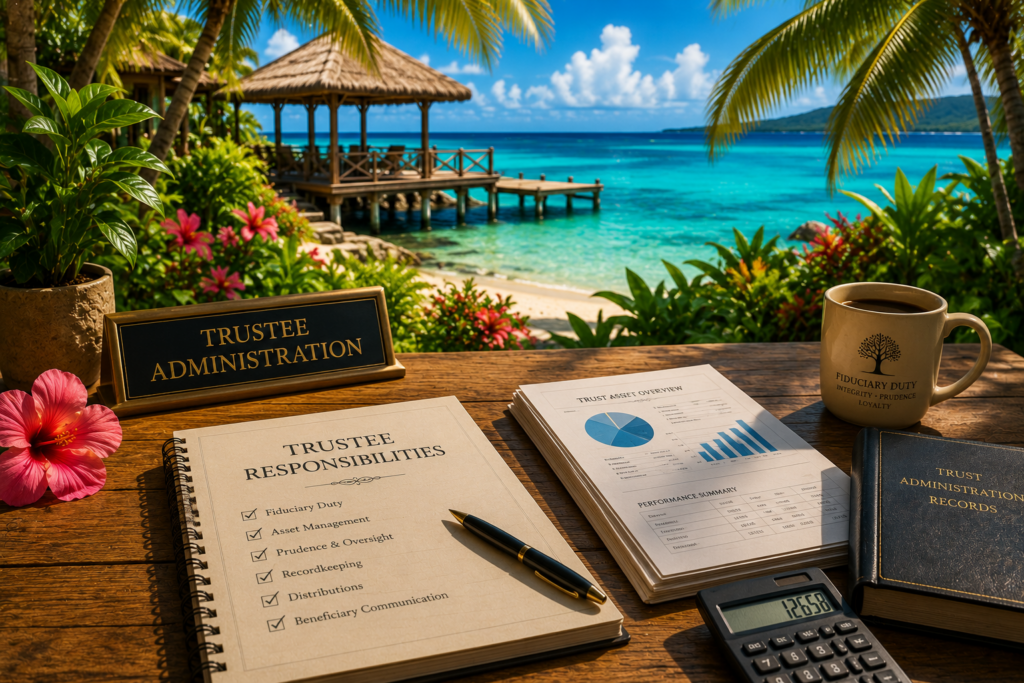

Trustees occupy fiduciary positions governed by some of the highest legal standards imposed under trust and estate law. Unlike ordinary financial relationships, fiduciary administration requires trustees to manage trust assets not for personal benefit, but for the benefit of the beneficiaries and according to the terms established within the trust agreement itself. This fiduciary relationship creates legally enforceable duties requiring the trustee to act with loyalty, prudence, neutrality, honesty, and disciplined administration throughout the life of the trust. The trustee therefore functions not merely as a manager of property, but as a legal steward responsible for preserving the operational integrity of the trust structure over time.

The duty of loyalty requires trustees to place the interests of the trust and its beneficiaries above personal interests or outside influences. Trustees generally may not use trust property for personal advantage, engage in self-dealing transactions, or favor their own financial interests at the expense of the beneficiaries unless specifically authorized by law or the trust terms. This duty becomes especially important in family trusts where trustees may also be beneficiaries, business partners, or close relatives of the individuals connected to the trust. Fiduciary law therefore imposes strict standards designed to prevent conflicts of interest from undermining the fairness and stability of trust administration.

The duty of prudence requires trustees to administer trust assets with reasonable care, sound judgment, and responsible financial oversight. Trustees are often expected to supervise investments, preserve property, coordinate taxes, maintain liquidity, oversee distributions, and manage long-term financial risks according to the objectives of the trust. This obligation does not require perfect investment performance or flawless business judgment, but it does require trustees to act thoughtfully, responsibly, and consistently with the level of care expected of a prudent fiduciary managing property for others rather than for personal ownership.

Neutrality and operational discipline further distinguish fiduciary administration from ordinary family decision-making. Trustees must often balance competing beneficiary interests across multiple generations while maintaining organized accounting records, preserving communication systems, coordinating banking authority, and following the operational requirements imposed by the trust structure itself. Emotional family pressures, informal agreements, or personal preferences cannot replace the trustee’s obligation to administer the trust according to fiduciary standards and long-term organizational stability. Trustees who neglect recordkeeping, act inconsistently, or abandon administrative discipline may expose both the trust and themselves to significant legal risk.

Ultimately, fiduciary duties exist to preserve confidence, accountability, and operational continuity within the trust administration process. Trust beneficiaries frequently depend upon trustees to manage property responsibly across periods of incapacity, death, and long-term succession planning. The fiduciary framework therefore imposes legal obligations designed to ensure trustees exercise authority carefully, transparently, and consistently with the purposes of the trust. Without these duties of loyalty, prudence, neutrality, and disciplined administration, the trust structure itself would lack the organizational safeguards necessary to preserve long-term stability and protect beneficiary interests across future generations.

The effectiveness of a trust depends heavily on long-term administration and organizational stability.

The long-term effectiveness of a trust depends not solely upon the legal document itself, but upon the quality of the administration, operational discipline, and organizational stability supporting the trust structure over time. Many individuals mistakenly believe that once a trust is signed, the planning process is essentially complete. In reality, trusts function as ongoing fiduciary systems requiring continuous coordination between trustees, financial institutions, asset management procedures, tax reporting systems, beneficiary relationships, and succession planning frameworks. Without proper long-term administration, even a carefully drafted trust may gradually lose effectiveness as operational inconsistencies and organizational weaknesses begin undermining the structure from within.

Organizational stability is particularly important because trusts often continue operating across multiple decades and generations. During that time, assets may change substantially, family dynamics may evolve, beneficiaries may experience different financial circumstances, and fiduciary responsibilities may transfer to successor trustees. Real estate may require long-term management, investment portfolios may need ongoing supervision, businesses may face leadership transitions, and tax obligations may continue changing over time. The trust therefore depends upon organized administrative systems capable of adapting to these developments while preserving continuity and maintaining compliance with the trust’s governing structure.

The role of fiduciary administration becomes critically important in preserving this operational stability. Trustees must maintain accounting records, supervise trust assets, coordinate banking authority, oversee distributions, preserve liquidity, communicate appropriately with beneficiaries, and document fiduciary decisions consistently throughout the administration process. Informal management practices, inconsistent recordkeeping, or operational neglect may weaken the trust gradually even where the legal documents remain technically valid. Many trust disputes arise not because the trust itself was defective, but because the administrative systems supporting the trust were poorly maintained over time.

Long-term organizational discipline also protects beneficiaries by reducing uncertainty and preserving confidence in the administration process itself. Beneficiaries often depend upon the trust structure to preserve continuity during periods of incapacity, death, financial transition, or generational succession. If trustees fail to maintain organized operational systems, beneficiaries may encounter confusion regarding distributions, asset management, ownership records, or fiduciary authority. Weak administration can create delays, increase legal exposure, destabilize family relationships, and expose the trust to unnecessary operational risk even when the original estate planning objectives were sound.

Ultimately, trusts operate most successfully when they are treated as active governance systems rather than passive legal documents. The trust structure depends upon long-term administrative coordination, disciplined fiduciary oversight, and organized operational management in order to preserve continuity across future generations. Proper administration allows the trust to fulfill its intended purpose by maintaining stability, protecting assets, coordinating succession, and carrying out the grantor’s instructions consistently over time. Without strong organizational systems supporting the structure, the practical effectiveness of the trust may deteriorate regardless of how sophisticated the legal drafting may have originally been.

Core Trust Components

The Essential Elements of a Trust Structure

Grantor Authority

The grantor establishes the trust and defines the legal instructions governing how trust property will be managed, administered, and distributed. The structure of the trust originates from the grantor’s intent and long-term planning objectives.

Trustee Administration

The trustee assumes fiduciary responsibility for managing trust assets according to the terms of the trust agreement and applicable law. Trustees are required to act with loyalty, prudence, neutrality, and disciplined oversight throughout the administration process.

Beneficiary Interests

Beneficiaries possess the equitable right to receive financial benefits from the trust according to the instructions established within the trust structure. Their rights and distributions are governed by fiduciary administration rather than direct ownership of the assets.

Trust Property

Trust property consists of the assets legally transferred into the trust, including real estate, businesses, investments, financial accounts, and personal property. These assets remain subject to the authority and operational management of the trust structure itself.

Understanding How Trust Systems Function

Trust Structure Principles

Trusts operate through a coordinated legal and fiduciary framework designed to manage property, preserve continuity, and carry out the grantor’s instructions over time. The effectiveness of the structure depends upon proper administration, organized asset management, and clearly defined fiduciary responsibilities between the parties involved in the trust. These foundational principles help explain how trusts maintain operational stability during life, incapacity, death, and long-term succession planning.

Administrative Authority

Trust administration depends upon the trustee’s ability to manage assets, maintain records, oversee distributions, and preserve operational continuity according to the terms of the trust agreement. Fiduciary authority allows the trust structure to continue functioning even during periods of transition or incapacity.

Asset Protection & Continuity

Trust structures help preserve continuity for real estate, financial accounts, investments, and multigenerational property holdings by centralizing management authority within the trust itself. Proper administration reduces operational instability and helps maintain long-term organizational structure over time.

Beneficiary Rights & Distributions

Beneficiaries receive financial benefits according to the instructions established within the trust agreement rather than through direct ownership of the assets themselves. Fiduciary administration governs how distributions occur, how trust property is managed, and how beneficiary interests are protected throughout the administration process.

Trust Structure Fundamentals

Understanding the Core Functions of a Trust

A trust operates through a coordinated legal structure designed to manage property, preserve continuity, and carry out instructions established by the grantor over time. The effectiveness of the trust depends upon proper funding, fiduciary administration, beneficiary coordination, and long-term operational stability. Understanding these foundational concepts helps explain how trusts function not merely as documents, but as organized systems for managing assets, protecting interests, and supporting succession planning across future generations.

Legal Authority & Trust Instructions

The legal authority of a trust originates from the written trust agreement itself, which establishes the operational framework governing how property will be managed, administered, protected, and distributed over time. The trust document serves as the controlling legal instrument that defines the rights, responsibilities, powers, limitations, and fiduciary obligations applicable to the parties involved in the trust structure. Unlike informal family understandings or verbal intentions, a properly drafted trust creates enforceable legal instructions capable of directing fiduciary administration during life, incapacity, death, and long-term succession planning. The effectiveness of the trust therefore depends heavily upon the clarity, organization, and legal precision of the instructions contained within the governing document.

Trust instructions define the scope of authority granted to the trustee and establish the operational standards governing administration of the trust property. These provisions may determine how assets are invested, when distributions may occur, how beneficiaries are treated, whether successor trustees may be appointed, and how property should be managed during periods of incapacity or after death. The trust agreement may also establish restrictions, conditions, discretionary powers, or protective provisions designed to preserve continuity and reduce future disputes among beneficiaries or fiduciaries. Because trusts frequently operate across long periods of time and multiple generations, the governing instructions must often anticipate changing financial circumstances, family dynamics, administrative transitions, and legal obligations that may arise in the future.

The distinction between legal ownership and fiduciary authority further emphasizes the importance of trust instructions within the administration process. Trustees generally do not manage trust assets as unrestricted personal owners, but instead administer the property according to the powers and limitations imposed by the trust agreement and applicable fiduciary law. Even where trustees possess broad discretionary authority, that authority remains legally connected to the purposes of the trust and the obligations owed to the beneficiaries. As a result, the written instructions within the trust document become the primary framework through which fiduciary authority is interpreted, exercised, and enforced over time.

Clear legal instructions are also essential for preserving administrative stability during periods of incapacity, death, or succession transition. When trust provisions are vague, internally inconsistent, or poorly organized, trustees and beneficiaries may encounter uncertainty regarding distribution standards, fiduciary authority, asset management responsibilities, or succession procedures. Ambiguity within the trust document can increase the likelihood of litigation, operational disruption, beneficiary conflict, and judicial intervention. Conversely, carefully drafted trust instructions provide organizational clarity capable of supporting efficient administration while reducing uncertainty throughout the life of the trust structure.

Ultimately, legal authority within a trust derives not simply from the existence of the trust itself, but from the operational instructions governing how the fiduciary system is intended to function over time. The trust agreement serves as the legal foundation upon which fiduciary administration, beneficiary rights, asset management, and succession planning are constructed. Properly organized trust instructions allow the structure to preserve continuity, maintain stability, and carry out the grantor’s intentions with consistency across future generations.

Trust Funding & Asset Coordination

The effectiveness of a trust depends heavily upon whether property has been properly coordinated with the trust structure through legally recognized transfer procedures. Trust funding refers to the process of transferring ownership, title, beneficiary designation, or legal control of assets into the trust so the trustee possesses authority to administer the property according to the trust instructions. Many individuals mistakenly assume that signing a trust document alone automatically subjects all assets to the trust structure. In reality, a trust may exist legally while remaining operationally ineffective if the property intended to be governed by the trust was never formally transferred into the fiduciary system itself.

Asset coordination involves aligning ownership structures, financial accounts, real estate interests, business holdings, investment portfolios, and beneficiary designations with the operational framework established by the trust agreement. Different categories of property often require different transfer procedures depending upon the legal characteristics of the asset involved. Real estate generally requires recorded deeds transferring title into the trust, financial accounts may require ownership changes or trust registration with the institution, and business interests may require assignments or amendments to governing documents recognizing the trust’s ownership rights. Failure to complete these coordination steps properly may leave significant assets outside the authority of the trust despite the grantor’s original planning intentions.

The funding process is critically important because trustees derive their administrative authority primarily from the trust’s ownership interest in the assets themselves. If property remains titled solely in the personal name of the grantor or another individual, the trustee may lack the legal authority necessary to manage, distribute, refinance, sell, or administer the asset under the trust structure. During incapacity or after death, these operational gaps frequently create delays, probate exposure, title complications, banking restrictions, or uncertainty regarding fiduciary authority. Families often discover these problems only after a crisis occurs, when improperly coordinated assets prevent the trust from functioning as intended.

Trust funding also supports long-term continuity by centralizing management authority within an organized fiduciary system capable of surviving incapacity, death, and generational transition. Real estate holdings, business operations, investment accounts, and multigenerational property structures often require ongoing supervision, payment obligations, financial oversight, and operational management regardless of whether the original grantor remains capable of exercising personal control. Proper asset coordination allows successor trustees to continue administering these systems without requiring immediate court intervention or fragmented ownership transitions that may destabilize the administration process.

Ultimately, trust funding transforms the trust from a theoretical legal document into an operational structure capable of exercising meaningful authority over the property it was designed to govern. Coordinating assets with the trust preserves continuity, supports fiduciary administration, and allows the structure to carry out the grantor’s long-term objectives with greater organizational stability. Without proper funding and asset coordination, even a carefully drafted trust may fail to provide the operational protection, continuity, and administrative efficiency it was intended to achieve.

Fiduciary Duties & Trustee Responsibilities

Trustees occupy fiduciary positions that carry some of the highest legal obligations recognized under trust and estate law. Unlike ordinary property managers or personal financial advisors, trustees administer trust assets on behalf of beneficiaries and according to the instructions established within the trust agreement itself. The trustee therefore functions not as an unrestricted owner of the property, but as a fiduciary charged with preserving, managing, protecting, and administering the trust assets in a manner consistent with both the governing trust terms and applicable legal standards. This fiduciary relationship imposes legally enforceable duties requiring trustees to act with loyalty, prudence, neutrality, honesty, and disciplined oversight throughout the administration process.

One of the trustee’s primary obligations is the duty of loyalty, which requires the trustee to prioritize the interests of the trust and its beneficiaries above personal interests or outside influences. Trustees generally may not use trust property for personal benefit, engage in self-dealing transactions, or favor one beneficiary improperly at the expense of others unless specifically authorized by the trust agreement or applicable law. Because trustees often possess substantial authority over financial assets, distributions, investments, and property management decisions, fiduciary law imposes strict standards designed to prevent conflicts of interest from undermining the integrity of the trust administration process.

The duty of prudence further requires trustees to exercise reasonable care, sound judgment, and responsible financial management when administering trust property. Trustees may be responsible for supervising investment portfolios, preserving real estate, maintaining liquidity, coordinating taxes, managing businesses, overseeing distributions, and maintaining organized accounting systems over extended periods of time. While trustees are not expected to guarantee perfect financial results, they are generally required to administer the trust with the level of care expected of a prudent fiduciary managing property for the benefit of others rather than for unrestricted personal ownership.

Trustees also carry substantial administrative responsibilities necessary to preserve operational continuity within the trust structure. These duties may include maintaining records, communicating appropriately with beneficiaries, documenting fiduciary decisions, preserving asset inventories, coordinating professional advisors, and ensuring compliance with the trust instructions over time. Failure to maintain organized administration may expose the trust to operational instability, beneficiary disputes, financial mismanagement, tax complications, or legal liability. In many trusts, the long-term effectiveness of the structure depends heavily upon the trustee’s ability to preserve disciplined oversight across changing financial and family circumstances.

Ultimately, fiduciary duties exist to preserve confidence, accountability, and continuity within the trust system itself. Beneficiaries often depend upon trustees to administer trust property responsibly during periods of incapacity, death, succession transition, and long-term multigenerational planning. The trustee’s fiduciary obligations therefore serve as the legal foundation supporting the stability and integrity of the trust administration process. Without disciplined fiduciary oversight, the trust structure may lose the organizational protections and continuity it was specifically designed to provide.

Beneficiary Rights & Distribution Structure

Beneficiaries hold the equitable interest within a trust structure, meaning they possess the legal right to receive benefits from the trust according to the terms established by the grantor. Unlike direct owners of property, beneficiaries generally do not control the day-to-day management or administration of trust assets unless the trust specifically grants them such authority. Instead, their rights arise through the fiduciary relationship governing the trust itself. This distinction between beneficial interest and operational control is one of the defining legal characteristics of trust law because it allows the trust structure to preserve organized administration while still protecting the financial interests of the beneficiaries over time.

The distribution structure established within the trust agreement determines how, when, and under what conditions beneficiaries may receive financial benefits from the trust property. Some trusts authorize mandatory distributions according to fixed schedules or percentages, while others grant trustees discretionary authority to evaluate distributions based upon health, education, support, maintenance, financial need, or long-term preservation objectives. The trust may also impose restrictions designed to preserve assets across generations, protect vulnerable beneficiaries, or prevent premature dissipation of wealth. These distribution provisions help ensure the trust operates according to the grantor’s intentions rather than solely according to immediate beneficiary demands or changing family pressures.

Beneficiary rights often include access to certain trust information, accounting records, and fiduciary reporting necessary to preserve transparency within the administration process. Trustees generally owe duties to administer the trust honestly, prudently, and consistently with the governing trust instructions, and beneficiaries may possess legal standing to challenge fiduciary misconduct, improper administration, or violations of the trust terms. However, beneficiaries are not typically entitled to exercise unrestricted authority over trust assets merely because they expect to receive future distributions. The trust structure intentionally separates fiduciary management from beneficial enjoyment in order to preserve continuity and organized administration over time.

Distribution structures become especially important in multigenerational trusts or trusts intended to operate long after the original grantor’s death. Trustees may need to balance the interests of current beneficiaries against future beneficiaries while preserving liquidity, investment stability, tax efficiency, and operational continuity within the trust system itself. Beneficiaries may possess differing financial needs, levels of responsibility, or long-term planning objectives, requiring trustees to exercise fiduciary judgment carefully when administering discretionary distributions. The distribution framework therefore serves not merely as a payment mechanism, but as a governance system designed to preserve fairness, continuity, and organizational stability across future generations.

Ultimately, beneficiary rights and trust distributions are governed through the legal and fiduciary structure established by the trust agreement itself rather than through unrestricted personal ownership of the assets. This framework allows trusts to preserve long-term oversight, protect vulnerable interests, coordinate succession planning, and maintain continuity during periods of incapacity, death, and future administration. By separating operational control from beneficial enjoyment, trusts create organized systems capable of carrying out the grantor’s intentions while balancing the financial interests and protections of the beneficiaries over time.

Continuity During Incapacity & Succession

One of the primary operational advantages of a trust structure is its ability to preserve continuity during periods where the original grantor is no longer capable of managing personal or financial affairs independently. Incapacity, illness, disability, or death can create significant disruption when property remains held solely through direct personal ownership because legal authority over the assets may become uncertain or require court-supervised intervention before administration can continue. A properly structured and funded trust reduces this instability by establishing a preexisting fiduciary system capable of continuing management authority through successor trustees according to the trust instructions already in place.

The continuity framework within a trust is designed to allow the administration of assets, businesses, investments, and property holdings to continue without interruption despite changes in the grantor’s personal condition or legal capacity. Successor trustees may assume fiduciary authority according to procedures established within the trust agreement itself, allowing financial obligations to continue being managed, investments to remain supervised, property to remain maintained, and operational systems to remain stable during periods of transition. This continuity is especially important for estates involving active business operations, multigenerational property holdings, investment portfolios, or complex financial structures that require ongoing administration regardless of the grantor’s personal circumstances.

Incapacity planning is often one of the most overlooked yet operationally significant functions of a trust. Many individuals focus primarily on post-death inheritance planning while underestimating the financial and administrative disruption that can arise during periods of diminished capacity. Without coordinated fiduciary systems already established, families may encounter delays accessing financial accounts, uncertainty regarding management authority, or court proceedings necessary to appoint legal representatives capable of managing the property. Trust structures help reduce these risks by preserving an organized governance system that may continue functioning without immediate judicial involvement.

Succession continuity after death also depends heavily upon the trust’s operational framework. Because trust assets are already subject to fiduciary administration prior to death, successor trustees may continue managing property according to the trust instructions without necessarily requiring probate administration for those specific assets. Real estate, businesses, financial accounts, and investment structures may therefore continue operating under centralized fiduciary oversight while distributions, tax obligations, creditor issues, and long-term succession planning are administered within the trust system itself. This continuity can help preserve organizational stability during periods where families are already facing emotional and financial transition.

Ultimately, continuity planning within a trust serves to preserve operational order, fiduciary authority, and long-term organizational stability across periods of incapacity, death, and future succession. Trusts function not merely as inheritance devices, but as ongoing governance structures designed to maintain management continuity when direct personal ownership alone may become operationally unstable. By establishing successor authority, fiduciary administration procedures, and coordinated asset management systems in advance, trusts help ensure that property and financial structures remain protected and functional despite changing personal or generational circumstances over time.

Long-Term Administration & Organizational Stability

The long-term effectiveness of a trust depends not merely upon the existence of a legally valid document, but upon the stability and organization of the administrative systems supporting the trust over time. Trusts frequently operate across many years or even multiple generations, requiring ongoing coordination between fiduciary management, financial oversight, accounting systems, beneficiary relationships, tax reporting, and operational continuity. A trust that lacks disciplined administration may gradually become unstable despite technically valid legal drafting because the surrounding organizational systems necessary to support the structure begin deteriorating over time. Long-term administration therefore serves as one of the central foundations preserving the practical effectiveness of the trust itself.

Organizational stability becomes especially important in trusts involving real estate, businesses, investment structures, or multigenerational property holdings requiring continuous oversight beyond the life of the original grantor. Trustees may be responsible for maintaining property, supervising financial accounts, coordinating taxes, preserving liquidity, documenting fiduciary decisions, and administering distributions over extended periods of time. These responsibilities often continue long after the original grantor is no longer capable of supervising the system personally. Without organized operational procedures already in place, the trust structure may encounter increasing administrative confusion, inconsistent management practices, or disruption during fiduciary transitions.

The administrative process also requires substantial coordination between legal authority and practical financial management. Trustees must maintain accurate accounting records, preserve asset inventories, communicate appropriately with beneficiaries, coordinate banking authority, and ensure compliance with the trust instructions throughout the administration period. Informal administration practices, undocumented distributions, poor recordkeeping, or inconsistent operational oversight may weaken the trust gradually by increasing uncertainty regarding fiduciary authority and financial accountability. Many trust disputes arise not because the trust document itself failed legally, but because the long-term administration lacked the organizational discipline necessary to preserve continuity and transparency.

Multigenerational trusts present additional complexity because future beneficiaries often inherit the consequences of administrative decisions made many years earlier. Real estate management strategies, investment decisions, discretionary distributions, tax coordination, and fiduciary oversight can all influence the long-term financial stability of the trust system across future generations. Strong organizational administration helps preserve fairness, operational continuity, and beneficiary confidence by creating reliable systems capable of surviving leadership transitions, changing economic conditions, and evolving family circumstances over time.

Ultimately, trusts function most effectively when they are treated as active governance systems requiring continuous administration rather than passive legal documents existing independently from the assets they control. Long-term organizational stability preserves the operational integrity of the trust by ensuring fiduciary authority, financial oversight, beneficiary coordination, and succession planning remain properly aligned across future years and generations. Without disciplined administration and organized management systems, the practical effectiveness of the trust may deteriorate regardless of how sophisticated the original estate planning structure may have been.

Learn More About Building Your Trust Strategy

For those who want to move beyond foundational trust education, additional guides and planning resources can provide deeper insight into trust structures, asset protection strategies, and long-term legacy planning. The following books and educational materials are designed to help expand your knowledge, strengthen your planning approach, and support the next step in building, protecting, or creating a trust strategy with greater clarity and confidence.

Revocable Trust

Flexible planning, lifetime control, and estate clarity

Irrevocable Trust

Long-term protection, structured preservation, and legacy security

Charitable Trust

Purpose-driven giving, strategic generosity, and lasting charitable impact

Asset Protection Trust

Strategic wealth protection, legal structure, and long-term asset preservation